How to fund your dream life, make work optional, and build a portfolio designed to last

Most people have the wrong definition of true financial freedom.

They think it means having enough to hopefully not go broke before they die.

But in my opinion, that’s planning for financial scarcity.

The real goal is stronger:

Build a portfolio designed to fund your dream lifestyle without requiring new contributions, while giving your wealth a reasonable chance to keep growing over time.

That is what I call Financial Escape Velocity.

The Rocket Analogy

In physics, escape velocity is the speed a rocket needs to break free from Earth’s gravity.

Below that speed, gravity wins. The rocket comes back down.

Your financial life works the same way.

Your spending is gravity. It pulls you back toward the job, the grind, and dependence on active income.

Your portfolio is the rocket. If it can’t support the cost of your life, you have to keep working to fund your lifestyle.

Once the portfolio becomes large and durable enough, the relationship can flip:

- Your investments can fund your lifestyle

- Work can become optional

- Your withdrawal rate can decline over a full market cycle

- Your wealth can keep compounding in your favor

That, to me, is financial freedom.

The Five Forces

A real rocket launch is shaped by several forces. Your financial rocket is too.

- Spending = Gravity. A more expensive lifestyle requires a larger portfolio.

- Investment Returns = Thrust. Returns determine how quickly the portfolio grows, but they never arrive in a smooth line.

- Portfolio Contributions = Fuel. The capital you add can shorten the journey.

- Time = Burn Time. Compounding becomes more powerful the longer it runs.

- Inflation = Drag. Rising costs increase the amount your portfolio must support.

Expected returns help estimate how quickly you might reach escape velocity.

Your planning withdrawal rate helps estimate how large the portfolio needs to be.

Mixing them creates a dangerously optimistic target.

Why I Don’t Love the Standard FIRE Definition

The FIRE movement, short for Financial Independence, Retire Early, helped a lot of people think more intentionally about money.

But it often aims at a lower standard than I want.

The common 4% rule starts with a first-year withdrawal equal to roughly 4% of the portfolio, then adjusts that amount for inflation. The original historical work tested whether a balanced portfolio could support about 30 years of withdrawals.

That’s a useful baseline. It isn’t a promise, and it doesn’t guarantee the portfolio keeps growing.

I want more margin. And while spending discipline helps, frugality is only one lever.

The fastest path usually combines smart spending with strong cash flow, high return-on-time activities, and intelligent asset allocation. Clipping coupons can only take you so far. Building a better machine creates a much bigger ceiling.

What Financial Escape Velocity Actually Means

Financial Escape Velocity is the point where your portfolio is large enough to support a reasonable planning withdrawal from your dream-lifestyle budget without depending on new contributions.

The stronger version has another feature:

Your spending becomes a smaller percentage of the portfolio over time.

That won’t happen every year. Bear markets can temporarily push the withdrawal rate higher. The real test is whether the rate trends lower across a full market cycle while your purchasing power holds up after inflation, taxes, and fees.

The Escape Velocity Portfolio Number

Most people know what they earn and what their mortgage costs. Few know how large their portfolio needs to be to fund the life they actually want.

Here’s the formula:

Escape Velocity Portfolio Target = Annual Dream Lifestyle Cost ÷ Planning Withdrawal Rate

The planning withdrawal rate is the percentage of the portfolio you expect to spend in the first year. It should reflect your time horizon, asset mix, flexibility, taxes, fees, and tolerance for bad market sequences.

Assume your dream lifestyle costs $120,000 per year:

- At a 4% planning withdrawal rate, the target is $3,000,000

- At 3.5%, the target is about $3,430,000

- At 3%, the target is $4,000,000

That range is more useful than pretending one return assumption can give you a precise answer.

Expected returns still matter. They help estimate when your portfolio might reach the target. They shouldn’t be used as the amount you assume you can safely spend every year.

A portfolio expected to average 6% won’t earn 6% on schedule. If you withdraw the full expected return, there’s no margin for inflation, taxes, fees, or a bad sequence of returns.

Dream Lifestyle, Not Survival Mode

Run the math using the life you genuinely want.

Where do you want to live? What will travel, healthcare, taxes, and irregular expenses cost? What does freedom cost for you?

Design the life you want, then build a portfolio with enough margin to support it.

Every extra $1,000 per month of recurring spending adds $12,000 to the annual budget. At a 4% to 3% planning rate, that can require roughly $300,000 to $400,000 more in portfolio value.

What the Napkin Math Misses

A simple target is useful, but life isn’t a spreadsheet. Account for:

- Inflation. At 3% inflation, a $100,000 lifestyle grows to roughly $134,000 in 10 years and $181,000 in 20.

- Taxes and fees. Portfolio returns and spendable cash aren’t the same thing.

- Sequence risk. A major drawdown during the first few years of withdrawals can hurt far more than the same drawdown later.

- Time horizon. Funding 50 years is a different problem from funding 20.

- Spending flexibility. Cutting optional spending during bad years can help.

- Large one-time costs. Healthcare, housing, family support, and major purchases need their own margin.

No calculator can promise the future. A useful one should show a range of outcomes and make its assumptions visible.

How You Actually Get There

Once you know the target range, the next question becomes obvious:

How do I build the machine that gets me there?

1. Maximize Cash Flow

Higher income, better margins, and scalable business models allow you to direct more capital into investments.

You need fuel for the machine.

2. Focus on High Return-on-Time Activities

Return on Time asks:

Which activities produce the greatest payoff for the least amount of time?

A wealth plan that owns all of your time has failed before the portfolio math even starts.

3. Optimize Asset Allocation

Asset allocation affects your expected return, volatility, drawdowns, taxes, and odds of surviving a bad sequence.

The job is to build an allocation you can hold through the ugly parts without permanently taking yourself out of the game.

Why Asymmetric Assets Matter

This is one reason I’ve spent so much time studying Bitcoin and other asymmetric opportunities.

When an asset dramatically outperforms traditional expectations, it can compress a journey that might have taken decades into years.

The other side is brutal volatility. Concentration can delay escape velocity or destroy the plan if the position is too large.

I’d rather build the base target with conservative assumptions and treat asymmetry as potential upside. Position sizing and diversification still decide whether you stay in the game.

The Perpetual Wealth Machine

My framework is simple:

- Maximize cash flow

- Channel that cash flow into investments

- Build a portfolio capable of funding your life

- Keep enough margin for the portfolio to compound

Cash flow becomes capital. Capital becomes assets. Eventually, the machine can support your life without constant labor.

What Changes Once You Hit Escape Velocity

The biggest shift is psychological.

Once your portfolio can fund your life, you can turn down bad opportunities, focus on projects that matter, and stop trading time for money on unfavorable terms.

Ironically, many people keep working after they hit escape velocity.

I did.

In fact, I work harder today than I did before hitting my number because I have the freedom to work on things I love.

The Real Standard: A Declining Withdrawal Rate

The 4% rule asks whether a portfolio has historically had a good chance of lasting through a conventional retirement.

My preferred standard asks more:

Can it fund the life I want while my withdrawal rate trends lower over time?

Some years will move in the wrong direction. That’s what markets do.

The goal is a portfolio where spending becomes a smaller percentage of the whole across full cycles. That’s real escape velocity.

Calculate Your Number

You can do the rough version on a napkin:

- Add up your annual dream-lifestyle spending, including taxes and irregular costs

- Choose a conservative planning withdrawal-rate range

- Divide annual spending by each rate

- Compare the target range with your current portfolio

Then use expected return, contributions, inflation, and time to estimate when you might cross the line.

Treat the result as a range. False precision is dangerous when markets don’t move in straight lines.

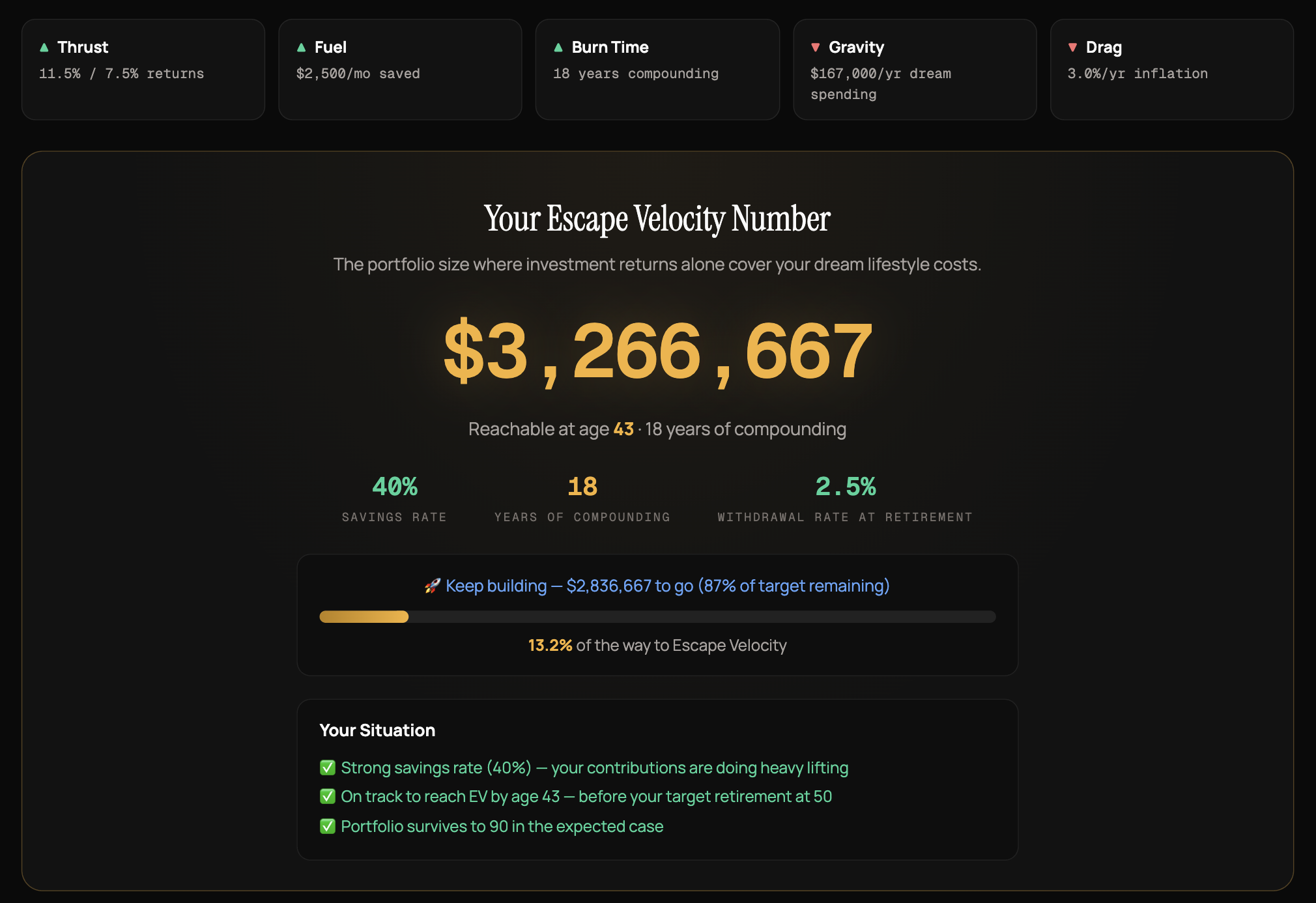

Want the real number? Run the free Escape Velocity Calculator →

It takes about 60 seconds. Plug in your current portfolio, income, spending, return assumptions, inflation, and target age. You’ll see your Escape Velocity number, how far along you are, and the projected path from here.

Once you know your range, the question changes:

How do I build the machine that gets me there?

The Mission

At Wealth Incubator, we help investors build portfolios designed to outpace the cost of their dream lives.

We want work to become optional, wealth to keep compounding, and freedom to become more durable.

Because the goal isn’t just to have money.

The goal is to build a portfolio powerful enough to break gravity.

This article is educational and reflects my personal framework. It isn’t individualized investment, tax, or financial advice. Assumptions and outcomes will vary.